Historical Crises & Monetary Policy- By Louay Chauki

- Laurier Economics Club

- Jul 8, 2021

- 6 min read

Introduction:

Bank of Canada’s principal role is “to promote the economic and financial welfare of

Canada”. It does so through influencing the money supply and the overnight interest rate to keep inflation low and stable. The Bank of Canada (BOC) has been a critical part of economic growth during times of contraction in Canada’s GDP. This literature will investigate the historical crises in Canada, such as the 2008 Financial Crisis and the 2015 Oil Crush, and the different monetary policies implemented to limit GDP contraction.

2015 Oil Crash:

Between 2014 and 2016, Canada had faced one of the largest oil price declines since 1986. Oil prices had dropped 70% from 2014 to 2016 and led to 45,000 people unemployed in Alberta. The Crude Oil Prices data shows a huge drop from 2014 to 2016 compared to 1986.

The decline in oil prices resulted from supply factors such as overproduction in U.S. oil, geopolitical concerns, and changes in the Organization of the Petroleum Exporting Countries (OPEC) regulations. The U.S. had produced 9.42 million barrels of oil per day reaching historical highs with Texas and Mexico producing over half of the barrels causing excess supply in the market. Also, there were geopolitical tensions in the Middle East and Russia. Saudi Arabia wanted to set a price floor for oil prices, but Iran and Russia were against so because the policy inflicted more damage to Iran and Russia than it did to Saudi. Lastly, OPEC decided to abandon price targeting in November 2015 which was a repetition of 1985-86 when oil prices crashed. OPEC began increasing the supply of oil and due to the policy change factor and as result oil prices plunged and stayed low for almost two decades. The lower oil prices reduced overall demand in the Canadian economy and put downward pressure on core inflation but managed to stay within the thresholds of 1% to 3% for most of the period.

The oil industry is a capital-intensive industry with lots of equipment and machinery needed in order to produce efficiently. International Energy Agency (IEA) said that global investment in oil and gas fell 25%. Below, the Canadian Investment growth dropped almost 7% in Q3 2015 which can spillover into GDP growth.

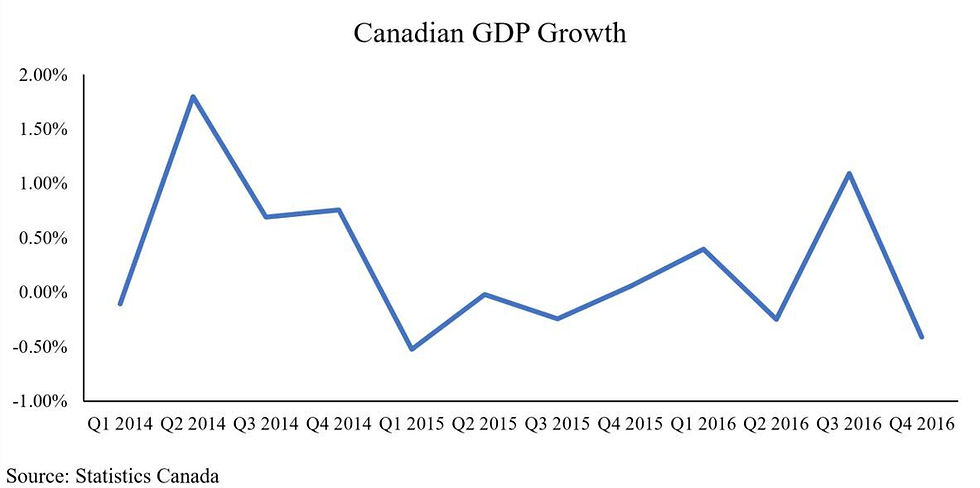

Due to declines in oil prices and investments, Canadian GDP growth declined in Q1 2015 after it peaked at 1.70% growth in Q2 2014.

In addition, as GDP growth declined, the Canadian Dollar (CAD) depreciated against most trading partner currencies. With a decrease in currency value, costs of imports for Canada raised significantly. The CEER versus major currencies dropped to historical lows of 103.97 showing significant depreciation in CAD.

With lower prices of oil, a decline in investments, and an increase in unemployment, BOC had noted that “The recent weakness in oil ... is likely to boost global growth for oil-consuming countries but to moderate growth and inflation in Canada, even though the effects should be tempered by exchange rate depreciation and stronger non-energy exports”. The BOC reacted to this crisis by cutting the overnight rate twice. Once in January and again in April 2015.

Governor Poloz mentioned that although the decrease in oil prices has negatively impacted the Canadian economy, it provided offsetting effects such as potential growth in Canada that other countries did not have. With depreciation in the CAD, other trading partners could benefit, such as the United States and China. Canada would be able to benefit and have an increase in exports contributing positively to the overall GPD. China would be able to purchase oil at a discount and United States would be able to purchase Canadian goods and services at a discount. As a result of the positive outlook, we see that there was limited monetary policy was needed for the 2015 oil crisis.

2008 Financial Crisis:

In October 2009, employment growth in Canada fell 4% from peaks in 2007. The 2008

Financial Crisis was caused by loose regulation in the financial industry, growth in securitization, conflicts of interest between Credit Rating Agencies and investors, and the too big to fail problem with financial institutions. Many of these were issues that occurred in the U.S. but had then spilled over to other countries such as Canada.

Loose regulations in the financial industry:

To begin, there were many firms that operated in fraudulent ways in order to maximize shareholder wealth and profits. The Securities Exchange Commission (SEC) had pursued few investigations and implemented little to no regulations for financial institutions on capital cushions relative to trades and balance sheets risk management or monitoring the derivatives market. Due to little regulations, many financial institutions were selling risky financial products to investors.

Securitization:

In order to increase profitability, many firms sold Collateralized Debt Obligations (CDO) or

Mortgage-Backed Securities (MBS) through the process of securitization. Securitization is the process of pooling various types of contractual debt such as credit card debt, automotive loans, and residential mortgages into a financial instrument that can be sold to institutional investors. CDO is a security backed by a diversified pool of a variety of debt obligations. MBS is a security backed by high-quality real estate mortgages. With the use of these securities, banks were able to increase funds available to lend which as a result increased liquidity and lowered costs of borrowing. But these securities were risky because the investors were being sold debt that was mixed of different ratings and investors were unaware that the debt many individuals took on with mortgages or credit card debt were unable to pay off with their income levels. This led to many defaults and losses on the MBS or CDO resulting in a domino effect. Many banks accumulated losses because the collaterals on the MBS or CDO’s were decreasing in value making it difficult to cover the loan given out.

Conflict of Interest:

One of the main reasons many investors accumulated losses was due to a false perception given by Credit Rating Agencies (CRA). CRA recognizes revenue when a company asks to be assessed in the scenario where they want to take on debt. The CRA then completes an evaluation of the company and provides an outlook. Through the evaluation,

they outline if the company is perceived as more or less risky. That is then factored into interest rates on debt and investor confidence. Due to the limited number of competitors, the CRA would provide an outlook that makes the company satisfied in order to ensure the company comes back. This causes a conflict of interest and deception to investors leading them to invest in companies that are riskier than indicated by the CRA.

Too big to fail:

When the household defaults started to kick in and banks suffered, many of them were going bankrupt as they were unable to meet debt obligations. Although they were about to go bankrupt, because they were a necessity to society and had a great impact on the financial markets as well as consumers, the government had come in and bailed most of the banks that were too big to fail. The government would provide financial support through loans, bonds, cash, or stock that may or may not have to be repaid. This kept financial institutions to stay afloat ensuring as minimal damage to the economy as possible.

Monetary policy response:

Due to the disastrous effect of the 2008 crisis with unemployment increases and

defaults on housing in the United States, one of Canada’s main trading partners,

BOC had cut the overnight rate from 4.5% in 2007 to 0.25% in 2009.

With changes in the target rate, we also see BOC had also increased money supply in 2009 in order to fight off the disinflation and achieve the 0.25% target rate.

BOC has also engaged in unconventional monetary policy such as organizing swap facilities,

expand on collateral opportunities ensuring liquidity within the market in order to stabilize the financial markets. Mark Carney Governor of the Bank of Canada in 2008 indicated “The intensifying financial crisis triggered a deep, synchronous global recession.”. But he also mentioned “Canada has suffered less than most other advanced economies ... Canada’s better performance can be explained by two factors. First, with a highly credible monetary policy and the strongest fiscal position in G-7”. With the use of fiscal and monetary policy, Canada was able to mitigate losses relative to other countries. Japan, European Union, and the United States faced negative growth in 2009, worse than Canada that only faced (2.00)% growth in 2009.

With significant disinflation due to high unemployment, lower housing prices, and individuals not able to pay or service their debt, inflation decreases past the lower 1% threshold at the beginning of 2009 and makes a swift recovery at the end of 2009.

Table 1 Source: Bank of Canada Monetary Policy Reports

Conclusion:

Based on the most recent historical contractions that Canada has faced, the BOC has been able to effectively recover the Canadian economy with the monetary policy toolkit provided. Based on the historical analysis, one can observe that overnight interest rates are used first

with money supply to deal with disinflationary and inflationary pressures. Alternative monetary policy is initiated as a last resort such as quantitative easing and introducing new initiatives such as forward guidance. In conclusion, monetary policy has been helpful

during times of contractions and there have been new innovative measures added to toolkits to adhere to BOC’s mandate.

Comments